The median sale price for single family homes in August saw an 11% year over year gain—but a lot of people last year said prices would go down. In fact, 1 in 4 people STILL think prices will go down. So what’s happening? (Tip: if you’d rather, I have a video version of this market report on my YT channel: search Jess Powers market update to find it)

The two questions everybody wants to know is: Will prices go down and will mortgage rates go down.

Whether you’re a potential homebuyer or seller, or just curious about the market, stick with me, because I’ve got a lot of valuable information to share. I’m going to dive into the third quarter, explore the factors shaping our market over the past few years, and discuss what’s in store for the future.

Let’s look at five data points that every buyer and seller needs to understand when trying to make sense of the current real estate market: Inventory, Equity, Mortgage Rates, Lending Standards, and Rental Prices.

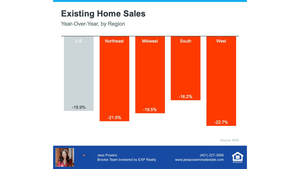

First let’s talk about Inventory: let’s break down the distinction between the number of homes available for sale vs the number of homes being sold. News sites are talking about how Nationally, home sales have seen a dip–however, that’s the number of homes sold, not prices. Sales are down because there are less homes available to be sold.

That’s an important distinction and data that could easily be distorted or misinterpreted. Meanwhile, home prices have gone up–even though many experts forecasted that prices in 2023 would go down.

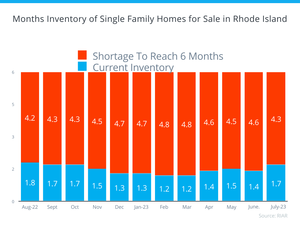

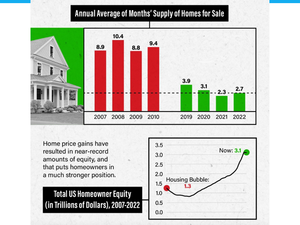

Let’s take a look at the inventory level of homes that are available for sale–Nationally, inventory levels hover around 3.3 months supply but here in Rhode Island, our inventory levels are critically low, sitting at 1.8 in August.

Housing Inventory levels in Rhode Island

To put that into perspective, at a National level the market could easily absorb double the current inventory.

So why are Inventory levels down? It’s pretty simple, there are three main factors at play: there aren’t enough new houses being built, people are staying in their homes longer, and many Sellers are reluctant to trade a low interest rate that they currently have for a higher interest rate so they’re not selling.

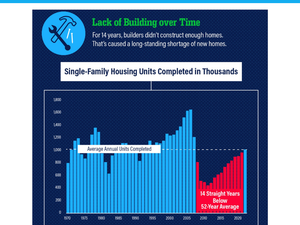

Let’s talk about homes being built:

We have a housing shortage across the US that started back in the Great Recession. There was a ten year period where the number of new homes being built was extremely low.

Here in Rhode Island, we’re extremely densely populated, and limited infrastructure has hindered new construction–we have many municipalities on septic systems and wells, you can’t just build a large development anywhere you choose, plus our zoning laws haven’t been revised to help alleviate the housing shortage. Rhode Island ranks dead last in the number of new construction homes being built.

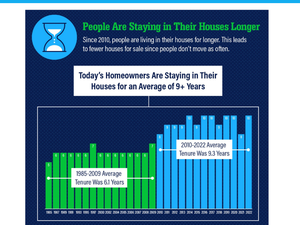

Now let’s talk about why people are staying in their homes longer: On average people used to stay in their homes about 5-7 years. Now folks are staying put, many choosing to renovate their homes rather than moving.

Astonishingly, 70% of homeowners with mortgages have locked in interest rates that are 4% or less.

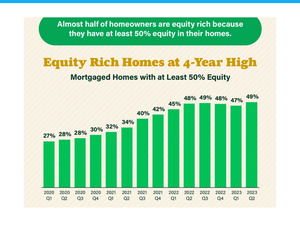

68% of those folks have paid off their mortgage or have at least 50% equity in their homes.

That’s leading to people staying in their homes longer.

The golden handcuffs of a low interest rate is playing out right now! But this is a double-edged sword because it’s likely that if rates are lowered they’ll be more favorable to buyers and sellers–and that may result in even higher prices. So sellers really need to evaluate how they can best leverage their equity right now vs waiting. If you own a home with a low interest rate and significant equity you may want to consider renting out that home—it’s expected that many will choose to do this, furthering our inventory issues.

Now let’s talk about Equity: Americans have been building substantial equity over the past several years.

Despite industry projections, prices have continued to appreciate Year-over-year, especially here in the Northeast. In August, our median sale price hit an all-time high of $450,000, marking an 11% year-over-year increase – a sign of a robust market.

So why do people continue to say that prices are going to drop?

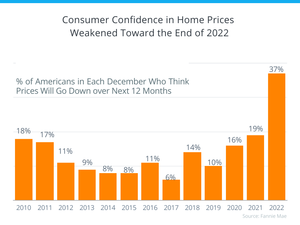

As I said in the beginning, at the end of last year, 37% of Americans expected housing prices to decline in 2023. This prediction isn’t new; it surfaces every year–seriously, there is someone saying the sky is going to fall in every single market.

2017–I had buyers saying they were waiting for prices to go down.

2019–saying they were waiting for prices to go down.

2020 when the pandemic shook the world–major fear that the housing market would crash.

2022 when interest rates spiked—the market’s going to crash…..and so on. But is that what the data is showing us?

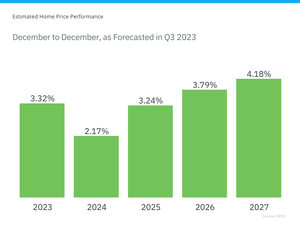

Many industry experts who had previously predicted that prices would go down have revised their forecasts, now foreseeing a period of appreciation over at least the next four years.

It’s essential to rely on facts. And the fact is that the available supply of homes is nowhere near the demand. And it would take a major economic crisis in order for that to change—either supply has to majorly increase or the demand has to plummet. And it’s highly likely that our government would step in to prevent a major crisis–coupled with the fact that because so many home owners have significant equity in their homes even if prices deflated a bit they would not be underwater. Plus we’re going to get to the fact that lending standards are significantly more stringent than ever before.

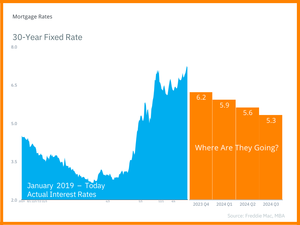

Now, briefly let’s talk mortgage rates.

I wish I had a crystal ball, but even experts have had to reevaluate their expectations. Rates remain uncertain, and inflation hasn’t gone down as quickly as hoped, resulting in rates continuing to rise. It’s so important to look at all of these details together in order to get a clear picture of what’s happening right now.

It was forecasted that rates would peak this past summer and go down this Fall but so far that’s not what has happened. Will they go down next year–historically rates do go down during election years but with this upcoming clown show, I’d say anything goes….

But what if rates reach 8% or higher? Interest rates can certainly cause the market to soften or even slightly deflate–we saw that last summer when rates spiked, but once buyers accepted that 6-7% interest rates were the “new normal” those that could still afford the monthly mortgage payments—or those that don’t even need a mortgage–have continued to buy and therefore prices have continued to increase. 8% or higher would likely cause the market to pause. Those who HAVE to sell could see their price go down but the fact is the market would likely become a stalemate.

We have two more data points to consider: mortgage lending standards and the rental market.

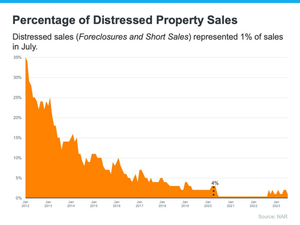

Mortgage credit availability is extremely stringent now, unlike the early 2000s when almost anyone could get a loan. Those lax standards were one of the main factors that led to the housing bubble–literally anyone could qualify for a loan or even multiple loans: no credit checks, no employment verification, loopholes for those with low credit scores. That’s just not the case for today’s lending standards.

Foreclosure rates in the US spiked in 2010 at 2.8 Million filings. Mortgage fraud, subprime mortgages– what a confluence of predatory lending standards that resulted in a significant number of people losing their homes. It led to a massive amount of available homes on the market – the opposite of what we’re experiencing now. It’s so important to look at all of these details together in order to get a clear picture of what’s happening right now. Compared to a decade ago, we have more stringent lending regulations, people with significant amounts of equity in their homes, and very few people who are delinquent on their mortgages.

I hope that you see from the information that we’re discussing—the low inventory due to a lack of sufficient homes being built, people staying in their homes longer, and folks with super low rates waiting to sell; the lending standards that make it much more difficult for people to qualify for loans and the low number of foreclosures and delinquency rates, that the conclusion that most are coming to–myself included–is that inventory is going to continue to remain low and therefore prices are going to continue to rise. Again, we could easily absorb double the inventory.

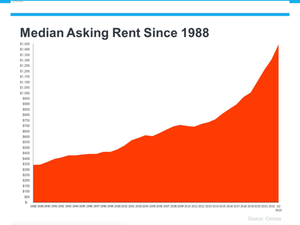

But we have one more metric to look at: Let’s talk about Rental Prices

Why? If you’re not going to buy real estate then you’re going to look for a rental so let’s quickly talk about the rental market.

My first apartment in Providence was a fabulous 3 bedroom in the Amrory District that I rented for $600 a month. Twenty years later and that same apartment now rents for $2200. In Providence the average 2 bedroom apartment is on the high side of $1800. If rental prices were still $1200 we would likely see more people opting to continue renting rather than buying their first home–that would certainly lower the demand side of the equation.

But with rents on the rise, renting as a long-term solution becomes less appealing–that’s why 27% of current home buyers are first time buyers.

Renters who are waiting for prices to come down could mean another 24k or more towards someone else’s mortgage…Four years later and they’ve spent nearly $100k and there’s zero return or equity on that money. It’s a cost analysis every renter needs to consider.

It’s not my job–or my intent– to convince someone to buy or sell real estate. My job is to serve as a guide and present the data to help my clients make informed decisions. And data is localized so while these national, regional, and state-wide numbers are important to understand you also need to really look closely at what’s happening at a detailed level.

The right time to buy is when the numbers work for you and align with your financial goals. If you try to time it based upon what a news outlet tells you then you’ll likely miss opportunities that could have been right for you because you misunderstood manipulated data aimed to scare you and sell ads.

Have questions? Let’s chat! If you prefer to watch this as a video then head over to my YouTube page!